Unlocking Top Magic Formula Stocks April 2024

Discover Bargain Opportunities in Quality Companies

Welcome to our newsletter, where we delve into Joel Greenblatt's Magic Formula and uncover some of the most promising stocks, along with a standout investment opportunity.

Joel Greenblatt's Magic Formula offers a straightforward approach to identifying undervalued companies. It begins by excluding utilities and financials, which tend to be unpredictable, leaving us with a curated list of 1,792 potential picks.

Next, it assesses the profitability of each company using a metric called Return on Assets (ROA). The formula then focuses on companies with the lowest Price-to-Earnings (PE) ratio, indicating potential bargains. Each company is assigned a score based on these criteria, with the one boasting the lowest total score considered the best investment opportunity according to the Magic Formula.

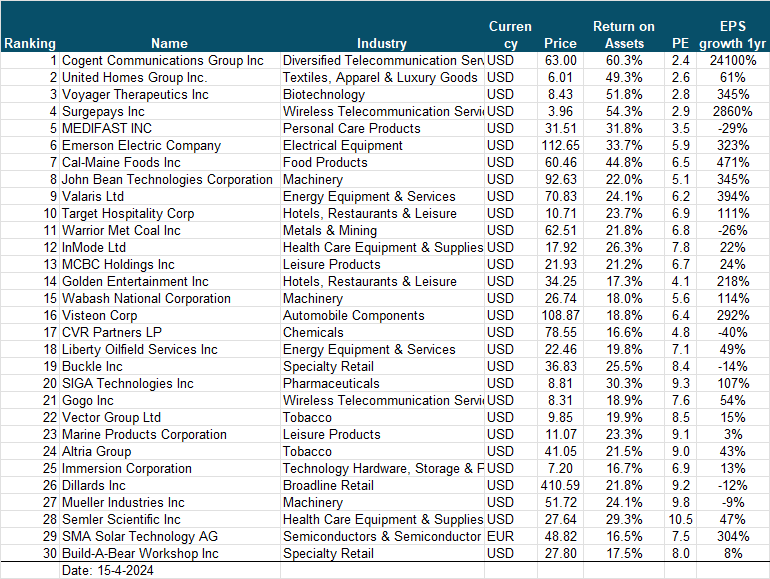

Additionally, we explored companies with very low PE ratios, such as Cogent Communications Group Inc and Surgepays, to determine their viability as investment options.

The ultimate goal is to identify companies that are performing well and are attractively priced. By following these steps, investors can construct a portfolio that outperforms the market over time. Greenblatt recommends selecting 6 or 7 stocks from the top 20 to 30 Magic Formula stocks to create a diversified portfolio with at least 20 stocks over several months.

The simplicity of this strategy appeals to many investors. While Magic Formula stocks historically outperformed the market, recent results have been less impressive. It's worth noting that the list often includes companies benefiting from one-time windfalls. Therefore, I personally use this screen as a starting point to uncover hidden gems.

Top 30 Magic Formula Stocks:

Now, let's take a closer look at four contenders:

1. InMode Ltd

Return on Assets (ROA): 26.3%

Price-to-Earnings (PE) ratio: 7.7

Analysis: InMode Ltd., renowned for its minimally invasive aesthetic medical products, demonstrates rapid growth and strong profitability, although growth is lowing down.

InMode's financial performance has been remarkable, with consistent revenue growth and expanding profit margins. With rapid growth, high profitability, a robust balance sheet, and apparent undervaluation, it presents an attractive investment prospect.

Valuation: InMode's valuation appears attractive relative to its growth prospects. Our DCF analysis shows a large Margin of Safety of 42% and the stock is cheaper than most similar companies. Despite its impressive performance, the stock trades at a reasonable Price-to-Earnings (PE) ratio 0f 7.7, suggesting potential upside for investors. That why I bought 300 Inmode stocks (2024-0416).

For a comprehensive analysis and valuation reports of Inmode, feel free to download our detailed report:

[Download Analysis and Valuation Report of InMode Ltd]

2. Emerson Electric Company:

Return on Assets (ROA): 33.7%

Price-to-Earnings (PE) ratio: 5.9

Analysis: Emerson Electric Co., a technology and software enterprise that offers Control Systems & Software across industrial, commercial, and consumer sectors. Emerson's performance has been buoyed by strong demand for its technology and software solutions, particularly in industrial automation and process control.

In 2023, the company witnessed a significant surge in net profit, soaring from $3,231 million in 2022 to $13,219 million. This boost was largely attributed to a profit of $11 billion from discontinued operations. However, when excluding this one-time sale, the adjusted earnings per share amounted to $4.44, contrasting starkly with the reported figure of $22.88.

Valuation: Considering this adjustment, the stock's Price-to-Earnings (PE) ratio stands at 25, indicating that it may not be undervalued despite the apparent increase in net profit.

This company shows one of the pitfalls of the simple Magic Formula framework. I observed that the list often includes companies benefiting from one-time windfalls.

3. Target Hospitality Corp

Return on Assets (ROA): 23.7%

Price-to-Earnings (PE) ratio: 6.9

Analysis: Target Hospitality Corp. specializes in rental and hospitality services, catering to government contractors and natural resource development companies. Target Hospitality's business model revolves around providing temporary housing solutions and support services to clients in.

Target anticipates total revenue for 2024 to range between $410 million and $425 million, contrasting with the $563.6 million revenue reported for the year ended December 31, 2023. Additionally, the company forecasts EBITDA for 2024 to be between $195 million and $210 million, compared to $344.2 million for the year ended December 31, 2023.

Valuation: Target has emerged from Joel Greenblatt's Magic Formula screen, suggesting that it is a favorable company trading at an attractive price. With robust profitability and a healthy balance sheet, Target stands out. However, projecting a decline in sales and profit for the upcoming year complicates valuation. Nevertheless, the company's current valuation remains reasonable when compared to historical metrics and similar firms. PE forward is 11.

[Download Analysis and Valuation Report of Target Hospitality Corp]

4. MCBC Holdings Inc

Return on Assets (ROA): 21.2%

Price-to-Earnings (PE) ratio: 6.4

Analysis: MasterCraft Boat Holdings, Inc. designs, manufactures, and markets recreational powerboats. It operates through MasterCraft, Crest, and Aviara segments. The MasterCraft segment produces premium recreational performance sport boats primarily used for water skiing, wakeboarding, wake surfing, and general recreational boating. The company is profitable with healthy margins and has a robust balance sheet. Earnings have been growing more than 12% per year the last 5 years, book value 30% and sales 16%.

Valuation: The company is trading at a 13% to 30% discount to historical valuation metrics averages. The PE ratio is is one of the lowest in the sector. Even in a no growth scenario the company has a Margin of Safety of 29% with our DCF analysis. My analysis of MasterCraft Boat Holdings is purely quantitative.

Investing in Magic Formula stocks requires diligence and a keen eye for value. As you explore these opportunities, remember to consider your investment goals and risk tolerance to make informed decisions.

Stay tuned for more insights and updates in our upcoming newsletters.

Kinds Regards,

Jasper Bronkhorst